The Major Behavioral Biases Influencing Your Investment Decisions

Posted by Jason Apollo Voss on Jan 14, 2020 in Blog | 0 commentsJason Voss recently spoke at the 2019 AAII Investor Conference. If you weren’t able to attend, session audio and handouts are available for purchase at:

Recognizing the major biases is the first step in learning how to avoid them in your investing.

You may not believe it, but science has proven that you and I are biased and often make irrational decisions. Here is the evidence.

Imagine a game pays $1.10 if a fair coin comes up heads and costs $1 if it comes up tails. You can participate in this game as often as you wish, as long as you hold up a dollar prior to each flip to ensure you are good for the potential loss.

Would you participate? For how many rounds? In answering this question, it might help to know that the expected return on each round is $0.05, or 5%, of your one dollar “investment.” (The math is $0.05 = [(0.5 × $1.10) + (0.5 × $1.00) – $1.00]). Does this change your decision regarding whether to participate?

Of course, you should play this game forever, as the expected return in each round is $0.05 and you will become hugely wealthy over time. But it turns out that very few of us would participate. This is because most of us experience far greater pain from losing one dollar than the joy we get from winning $1.10. What is more, the fact that the game can be played multiple times seems to have a limited impact on the decision. It appears we view each round as a separate event. This particular decision-making bias is known as “loss aversion,” and I discuss it more fully in the next section.

This result stands in stark contrast to that imagined by classic economists, who assume that all of us make perfectly rational decisions. Chances are that had any of the formulators of economic theory done a check with anyone other than the robotic folks who advanced their theory, those formulators would have known what we know. Namely, that all of us frequently make irrational decisions.

That we are all biased is interesting. But even more interesting is the question of how do we avoid these biases to become better investors?

The LOC HAARM Biases

Philosophers have, of course, noted bias in people’s thinking for thousands of years, but scientists in psychology only began formally researching bias in human decision-making in the 20th century. Since then well over a hundred different behavioral biases affecting decision-making have been identified, as documented on The Psy-Fi Blog and Wikipedia.

Of the formally identified biases, there are less than 10 that deserve the attention of investors. It isn’t that the others are unimportant, it is just that many of them are corollaries of these major biases:

- Loss aversion

- Overconfidence

- Confirmation

- Herding

- Anchoring

- Availability

- Representativeness

- Mental accounting

A helpful mnemonic device for remembering these biases is LOC HAARM, “brain LOCk that HAARMs investment performance.” Let’s take each of these biases in turn so that you can begin to recognize them in your own decision-making. In fact, it is instructive to think about these errors in judgment and relate them to your own investing history.

Loss Aversion

The most widely quoted finding of research done on loss aversion, sometimes known as myopic loss aversion, is that people generally experience the pain of loss more severely than they do the pleasure of gain. Simply stated, most of us would prefer to avoid a loss of $100 than we would to gain $100. Consequently, most people try to avoid personal harm or loss first, and seek pleasure second. In investing, this means we are likely to scrap our long investment time horizon if we begin experiencing losses.

How large must the return to “heads” in the coin toss game above be in order to attract the typical individual to play and keep playing? Research has shown that the amount is somewhere around $2, which means that the ratio of gain to loss is approximately 2-to-1. That is, short-term loss aversion is twice as strong a feeling as the positive feelings regarding a comparable-sized gain.

There is another aspect to loss aversion that is less widely understood. Namely, when given a choice between a) an 85% chance to lose $1,000 paired with a 15% chance to lose nothing and b) a sure loss of $800, a large majority of people choose option a. What is going on here? People are about 2:1 more risk averse except when they believe they have already lost almost everything. In these instances, we switch from being risk avoiders to being risk seekers!

Anxiety about loss, of course, finds a rich partner in investing, which has many possible sources of anxiety, right? Just think of how you feel when you read bad news about one of your investments. Ugh. Our temptation is to abandon ship and sell our interest in the business. However, we also can become “double-or-nothing” risk takers if we believe our investment is hopeless. I discuss this more in the section on anchoring.

Overconfidence

Cautions against overconfidence are millennia old, with admonishments about overconfidence being featured in Sun Tzu’s fifth century treatise, “The Art of War,” for example. Psychologists in the mid-20th century began formulating ways of testing for overconfidence, with papers appearing soon thereafter. Commonly, people are asked to assess their confidence in their knowledge about something that is verifiably correct.

Among many papers researching this issue, Adams and Adams in 1960 asked people their confidence in their ability to spell difficult words for a study published in The American Journal of Psychology. If people in the aggregate stated, for example, that they were 75% certain they could spell a difficult word, but in reality they only could do so 50% of the time, the difference is considered the degree of overconfidence.

Remember, again, that behavioral biases are universal. Thus, it is likely that you are overestimating your abilities as an investor, or of your understanding of key issues affecting your investments. Note: Because of the universality of overconfidence in all investors, checking your own and recognizing it in others is likely a rich source of alpha [return above your benchmark].

My Key Insights About Behavioral Finance

Based on my many years as an investor as well as a behavioral finance researcher and author, here are the key insights I have gathered:

Behavioral Biases Are not “Hard” Wired

Many of the psychologist progenitors of behavioral finance commit an error in judgment. Namely, they frequently say that the behavioral biases are “hard wired,” meaning that there is nothing that can be done under the sun to avoid and overcome them. If this were true then there would be no reason to go to school, and we would not have words for concepts like learning or change. All of us would be the same as we had been when we were born, and we would all behave with the impulses of children.

Instead, one of the strongest and most consistent findings of neuroscientists is the brain’s neuroplasticity. This is the remarkable ability of the human brain to change and adapt to new experiences. For the record, I believe that behavioral biases are very strong tendencies, just as behaviors themselves are very strong tendencies. However, people can and do change behavior.

Behavioral Finance Is a Diagnosis, not a Prescription

It is important to note that, for most, the insights of behavioral finance remain a diagnosis (“we are biased”) without much of a prescription (“here is what you do about it”).

Behavioral Biases Are One Bias

All behavioral biases are essentially the same error in judgment just expressed in different guises. Namely, behavioral biases are almost all the failure on the part of a decision-maker to recognize that there is a mathematically correct, or rationally correct, way to make an impending decision. Thus, if you can remember to apply the responsiveness of a decision needing to be made to either mathematics (including statistics) or rationality, then most of the biases can be avoided.

In other words, investment professionals need a way of inserting a pause between a stimulus … and … a response. Do this, and many of the behavioral biases are mitigated and maybe even avoided altogether.

—Jason Voss

Confirmation

Like our two preceding biases, confirmation bias is something that has been noted for thousands of years by commenters. Let’s let Thucydides, its oldest definer, have the floor: “… it is a habit of mankind to entrust to careless hope what they long for, and to use sovereign reason to thrust aside what they do not fancy.” More recently, “[Confirmation bias] connotes the seeking or interpreting of evidence in ways that are partial to existing beliefs, expectations, or a hypothesis in hand,” as explained by Raymond Dickerson in the Review of General Psychology. More colloquially, confirmation bias is described well by the old saying, “To the man with a hammer, every problem looks like a nail.”

Not surprisingly, investors are not immune from confirmation bias. Researchers studied investor behavior in South Korea and found that most investors on stock message boards displayed confirmation bias. Furthermore, they also found that those exhibiting greater confirmation bias also displayed the highest confidence in their decisions, too. This is an important point, as many of these biases interweave with one another and result in a sum-is-greater-than-the-parts effect. Ouch!

Herding

Surely you have heard about herding, and that market prices sometimes form speculative bubbles. Most famous in investing is Charles Mackay’s 1841 classic, “Extraordinary Popular Delusions and the Madness of Crowds.” A single quote from him should serve our purposes: “Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one.”

Yet, in a similar refrain to our other major behavioral biases, Mackay himself has been criticized as an ardent booster of multiple bubbles in his time as a journalist, including by the University of Minnesota’s Andrew Odlyzko. In other words, all of us are susceptible to behavioral bias, even if we are considered classic authorities on the subject.

In biology it has been noticed that when stampeding, each member of a herd reduces its own dangers by orienting itself as closely as possible to the center of the whole herd. This is an apt description of behavior in the midst of asset bubbles, where absolute notions of value and return are surrendered to relative notions. Here, participants crowd into individual securities or into markets to orient themselves, “as closely as possible to the center of the whole herd.” But they also do the same thing if there are dramatic drops in markets, too. Most investors do not want to be left behind or stampeded over.

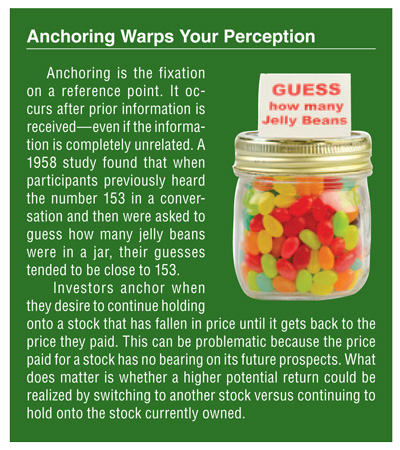

Anchoring

Anchoring is the fixation on a reference point within a continuum of information in decision-making. It was first described by psychologists in a 1958 issue of the Journal of Experimental Psychology. For example, researchers in an experiment will mention the number 153 randomly in conversation. Then later when asking a group to estimate the number of jelly beans in a jar, the group’s estimates anchor on the number 153. This is true regardless of which number is chosen.

A classic example of anchoring in investing is the cost basis we pay for an investment, where investors refuse to sell a security “until it gets back into the black.” What should always matter with an investment is its future prospect, and not what you paid for it. Recall our discussion about when risk aversion turns to risk seeking: If we anchor on our cost basis and have switched to a risk-taking mode, then it is likely we add to a losing position in an attempt at “double or nothing.”

What matters, though, is that if you believe that the return on capital going forward for a stock that has fallen in value is better than other investment prospects, then you continue to hold. If not, then it makes sense to sell, harvest the tax loss benefits and redeploy monies to a company whose stock you believe has better prospects.

Availability

How important is the price of gasoline as an economic issue? For some it is very important but for most it is not, although everyone—save for an oil company—would like to see a lower price. But if we watch the news, we would think it very important since its level is reported frequently, and it is often the topic of lengthy news stories.

The price of gasoline is an example of the availability bias. When asked to think about an issue, we often focus on what is most available to us at the time or can be most easily recalled. Another example is the level of the Dow Jones industrial average. We frequently place too much credence in its gyrations simply because its movements are widely reported.

Interestingly, a single reporting of an event may trigger the availability bias, while multiple reportings trigger an availability cascade. In such cases, multiple reports have an overpowering influence on individuals, driving them to make emotional decisions. See the section on herding. When a piece of information is in cascade mode, it is extremely difficult to come to an independent judgment because everywhere we turn the event is being reported and people are overwhelmed by the event.

Representativeness

Like much of behavioral economics, representativeness bias was first described by that dynamic duo, Amos Tversky and Nobel laureate Daniel Kahneman in their paper “Belief in the Law of Small Numbers” (Psychological Bulletin, 1971). Specifically they stated:

“We submit that people view a sample randomly drawn from a population as highly representative, that is, similar to the population in all essential characteristics. Consequently, they expect any two samples drawn from a particular population to be more similar to one another and to the population than sampling theory predicts, at least for small samples.”

Tversky and Kahneman provide an explicit example: “Steve is very shy and withdrawn, invariably helpful, but with little interest in people, or in the world of reality. A meek and tidy soul, he has a need for order and structure, and a passion for detail.”

In this kind of study, they then go on to ask participants the likelihood that Steve has a particular profession, such as farmer, salesman, airline pilot, librarian or physician. If you understand representativeness, then you likely guessed that most research subjects state that Steve is a librarian.

In other words, decisions are often made based on preferences and stereotypes, rather than on sound judgment. An example from investing might be a refusal to consider a growth stock with a high price-earnings (P/E) ratio because you are a “value investor.” In fact, value simply means that a security is fairly priced for the future growth prospects of the business.

Mental Accounting

Mental accounting may be described as the artificial compartmentalization of money into different categories and applying different decision rules to those categories. Richard Thaler, another Nobel Prize winner for his work in behavioral economics, was the first to formally describe mental accounting bias in a 1985 paper published in Marketing Science. He provided several salient examples demonstrating mental accounting, including: “Mr. and Mrs. L and Mr. and Mrs. H went on a fishing trip in the northwest and caught some salmon. They packed the fish and sent it home on an airline, but the fish were lost in transit. They received $300 from the airline. The couples take the money, go out to dinner and spend $225. They had never spent that much at a restaurant before.”

In this example the two couples clearly had compartmentalized the monies received from the airline as “house” money, and not as their own. Consequently, they spent more at the restaurant than they ever had before. The couples overlooked the fact that because money is fungible they really were spending their own money, not that of the airline. After all, they could have invested the money instead, or at long last fixed a broken house lamp.

To further illustrate, say we do not sell a corporate bond out of a portfolio because it is part of the diversified bond fund’s “long-term capital.” Instead we sell a better-performing bond out of the “short-term capital” portion of the portfolio, thus hurting returns. This is an example of mental accounting bias and its possible detrimental effects on investment returns.

Conclusion

You’ll benefit by keeping the LOC HAARM biases in mind as you tackle investment decisions. Be honest with yourself, as you are the only witness to these errors. Admitting that you are susceptible to behavioral biases is the first step to learning how to avoid them.

Originally published on the AAII homepage, an organization I wholeheartedly endorse.